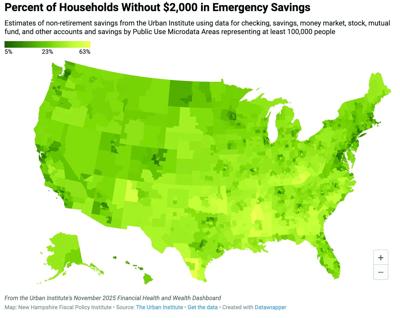

A broken furnace, medical bill, or car repair could quickly become a financial crisis if it were to happen in any one of over 120,000 New Hampshire households with very little savings. An analysis recently published by the Urban Institute found that nearly one in four New Hampshire households lacked at least $2,000 in non-retirement savings in 2022, representing a basic financial cushion for weathering emergencies. According to the analysis, about 23% of New Hampshire households did not have non-retirement savings, such as money in a checking or savings account, totaling more than $2,000 in 2022. That figure rose to 30% for Granite Staters in rural northern and western New Hampshire, 32% for Manchester residents, and 31% for Granite Staters of color statewide.

The Urban Institute published this analysis in November 2025 using the latest consistently available data for each type of financial well-being measured. A previous version of the analysis, published in 2022, found about 26% of New Hampshire households lacked $2,000 in emergency savings in 2019, although the $2,000 threshold was not adjusted for inflation between those two years. The researchers also measured overall wealth, income relative to key expenses, and certain other metrics.

Unpaid debt

Researchers at the Urban Institute also found that about 16% of Granite Staters had some form of debt that was at least 60 days past due in 2023. Two percent of all residents specifically had delinquent student loan debts.

Housing expenses

About 87% of all households with less than $50,000 in annual income, which was about one in four New Hampshire households in 2023, paid more than 30% of their incomes for their housing costs, such as rent or mortgage payments, utilities, property taxes, and insurance costs. For Granite Staters of color, about 96% of households with these lower incomes were cost-burdened, or paying at least 30% of income, by housing costs.

This percentage varied for different areas within the state as well. While about 78% of all residents with lower incomes in Coos, Grafton, and Sullivan counties combined were cost-burdened by housing, about 95% of Manchester residents and 91% of Strafford County and northern Rockingham County residents were cost-burdened in this manner.

Utility costs

About one in five New Hampshire households paid more than 10% of household income solely on utility costs, including electricity, water, gas, and heating fuels. While the lowest percentage of households facing these utility costs were near Nashua and a few other relatively urban parts of the state, about 46% of households in Coos, Grafton, and Sullivan counties, and 41% in eastern central New Hampshire encompassing Carroll and Belknap counties, paid more than 10% in utility costs.

Access to emergency savings varies

Savings can be difficult to accumulate for a variety of reasons, and the primary factors include income and expenses. Both lower incomes and higher expenses make saving more difficult, while their opposites enable more opportunities to set money aside for a time of need. Some of the variations in savings across New Hampshire could be rooted in both factors.

The approximately 23% of Granite State households without at least $2,000 in savings during 2022 represents about 129,600 households of the estimated 557,200 in New Hampshire that year. In Coos, Grafton, and Sullivan Counties, which include the two counties (Coos and Sullivan) with the highest poverty rates in the state, about 30% of households lacked that level of savings. Coos County also had a median household income that was only slightly more than half of Rockingham County in southeastern New Hampshire. The cost of buying a house has also increased fastest in rural parts of New Hampshire, although the overall cost is still lower than in southeastern New Hampshire.

In Manchester, where 32% of households did not have at least $2,000 in emergency savings (the highest rate of the measured areas in the state) in 2022, the cost of renting the median two-bedroom apartment increased 31% from 2020 to 2024 to $1,838 per month. Median household income, at about $77,000, was below the statewide median of about $95,600 during the 2019 to 2023 period. Increasing costs, particularly regional housing costs, likely made saving very difficult for households in Manchester and elsewhere, particularly the families that are more likely to see incomes fall short of expenses than ten years ago.

Wealth is a critical factor, difficult to measure

Most common measures of financial well-being are based on income. Income is often measured through surveys and tax returns, and income from employment is also reported by businesses and other employers. As a result, income is more commonly measured than wealth. Income measures the money coming into a household in a given time period, while wealth measures the assets owned by the members of a household.

Wealth provides a form of economic security that promotes resilience, including the ability to weather a job loss or an unexpected expense, such as a car repair or medical costs from an illness. Even a higher income does not provide the security of having a substantial amount of money in a bank account, as that income could change, or new costs could appear, relatively quickly. Wealth provides a financial cushion that can be critical for individuals and families in times of need.

Local data difficult to access

While national measures provide insights into wealth and wealth inequality, which has risen substantially over the last six decades, local data are much harder to collect than data about the income of residents in states and counties. Researchers at the Urban Institute used publicly-available data and collaborated with a major credit bureau, employing anonymized data, to get a sample of about 10 million people nationwide. They also utilized models to understand the likely conditions facing people in less-populated areas and in smaller population groups when the sample sizes themselves were too small to create reliable estimates.

These data and methods allowed the Urban Institute researchers to estimate the percentage of households that had less than $2,000 in their bank accounts, stocks, mutual funds, and other non-retirement assets. However, the data were not granular enough to allow for consistent town- or county-level analyses in New Hampshire. The data were organized by regions of the state (and country) with a total of 100,000 people or more. While data for Manchester can be separated from the rest of the state with this strategy, every other city or town is combined with at least one other community in these data.

Different than other surveys

This methodology is notably different from a commonly-cited national-level survey conducted by the U.S. Federal Reserve Board’s Survey of Household Economics and Decisionmaking, which asks U.S. residents nationwide a series of questions. These questions include asking about the methods the individual would use to pay for an unexpected $400 expense.

The latest survey indicates that 37% of U.S. adults would not have paid for an unexpected $400 expense with cash, savings, or a credit card to be paid off by the end of the month. While that indicates more than one in three U.S. adults do not have the savings to easily cover this expense, 13% said they would be unable to pay it by any means; others indicated they would carry a balance on a credit card, borrow money from a friend, family member, bank, or payday lender, or sell something to help pay for the expense. That suggests many adults would not spend their bank account down to zero, perhaps to preserve some wealth cushion for other unexpected expenses or to avoid fees.

While these survey data offer key insights and annual updates allowing for helpful comparisons over time, the Urban Institute’s methods seek to measure the actual balances in household accounts. The Urban Institute’s data also provide insights into the financial resilience of New Hampshire residents specifically.

Financial situations fragile for many Granite State families

Without $2,000 in savings, a Granite Stater could quickly spend their liquid assets to pay for an unexpected car repair, needed fixes for a house or an appliance, the deductible on their health insurance after an injury or illness but before coverage begins, losing a job, or other factors that could effectively require immediate, unforeseen costs. That would potentially lead to debt that could be difficult to pay off, unpaid bills, or forgone health or housing needs.

Housing, utility, health care, and child care costs have increased across New Hampshire. These rising costs have made building emergency savings increasingly difficult. With nearly one in four New Hampshire households in this fragile situation, small changes in physical or financial well-being, expenses facing families, public policy, or the economy overall could have big impacts on many Granite Staters.

•••

The New Hampshire Fiscal Policy Institute is sharing these articles with the partners in The Granite State News Collaborative. NHFPI is an independent nonprofit organization that explores, develops and promotes public policies that foster economic opportunity and prosperity for all New Hampshire residents. For more information visit nhfpi.org and collaborativenh.org.

(0) comments

Welcome to the discussion.

Log In

Keep it Clean. Please avoid obscene, vulgar, lewd, racist or sexually-oriented language.

PLEASE TURN OFF YOUR CAPS LOCK.

Don't Threaten. Threats of harming another person will not be tolerated.

Be Truthful. Don't knowingly lie about anyone or anything.

Be Nice. No racism, sexism or any sort of -ism that is degrading to another person.

Be Proactive. Use the 'Report' link on each comment to let us know of abusive posts.

Share with Us. We'd love to hear eyewitness accounts, the history behind an article.